Hydrogen Has Not Lost Momentum—It Has Been Misplaced Why the "Hydrogen Ladder" Has Sparked a Global Debate, and What It Means for Taiwan

Hydrogen Has Not Lost Momentum—It Has Been Misplaced Why the "Hydrogen Ladder" Has Sparked a Global Debate, and What It Means for Taiwan

by Martin Tsou[1], Advisor, Chung-Hua Institution for Economic Research (CIER),

& Jong-Shun Chen[2], Associate Research Fellow, Chung-Hua Institution for Economic Research (CIER)

In recent years, global hydrogen development has entered a visible "cooling phase." After governments around the world announced ambitious national hydrogen strategies, an increasing number of large-scale projects have been delayed, downsized, or cancelled due to escalating costs, unclear demand signals, and heightened investment risks. As a result, the international debate has shifted—from whether hydrogen can support net-zero transitions to where hydrogen should be used first under conditions of limited supply and high cost.

It is within this context that energy transition expert Michael Liebreich introduced the concept of the Hydrogen Ladder, which has since triggered extensive global discussion. The core message of the Hydrogen Ladder is not to dismiss hydrogen as an energy solution, but rather to emphasize a fundamental reality: clean hydrogen is scarce, and misallocating it may prove more costly than not using it at all.

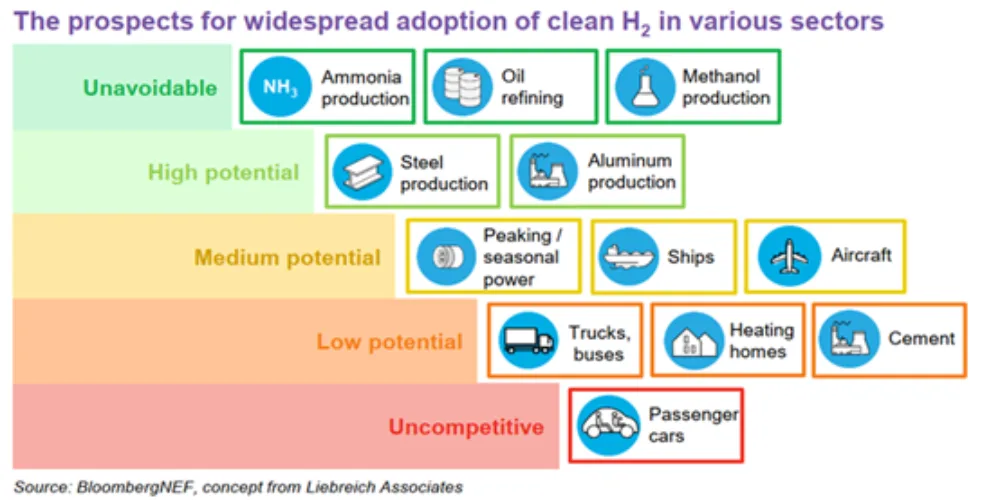

Hydrogen Ladder of Michael Liebreich

Hydrogen: Allocating Scarce "Clean Hydrogen" to Where It Creates the Greatest Value

Hydrogen is an energy carrier with significant potential, but it is not a universal solution. More precisely, clean hydrogen is scarce. At a stage where renewable electricity still needs to scale up, carbon capture and storage (CCS) has yet to be fully deployed, and supporting infrastructure remains insufficient, the availability of clean hydrogen that can be supplied at low cost and with low carbon intensity is inherently limited. This implies that, if Taiwan is to deploy hydrogen effectively, it must adhere to a fundamental principle: scarce resources should be prioritized for applications with high value added, limited direct electrification alternatives, and a clear structural necessity for decarbonization.

Over the past few years, hydrogen was once widely regarded as a "key solution" for the energy transition. Against the backdrop of net-zero commitments and geopolitical dynamics, governments around the world introduced national hydrogen strategies, while industry responded with large-scale demonstration projects and long-term investment roadmaps. However, as projects began to enter the commercial phase, practical constraints gradually became evident. Higher-than-expected costs, the absence of mature demand, and slow infrastructure deployment have led many highly anticipated hydrogen projects to be delayed, scaled back, or even cancelled altogether. Consequently, the tone of international hydrogen discussions has shifted from "full-scale deployment" to "strategic recalibration."

Indeed, global hydrogen development is cooling, and the debate is no longer centered on technology. Importantly, this "cooling" does not signify the failure of hydrogen. Rather, it reflects a growing recognition that the core issue is not whether hydrogen can be used, but whether it is being applied in the right place. As renewable energy continues to expand, CCS remains incomplete, and transport and storage infrastructure is still being built, the ability to supply clean hydrogen at low cost and with low emissions is itself a constraint. Under such conditions, the absence of clear prioritization risks turning hydrogen into yet another over-promised but under-delivered transition slogan.

It is precisely within this international context that energy transition expert Michael Liebreich proposed—and has continued to refine since 2021—the concept of the Hydrogen Ladder. This framework seeks to answer a critical question in a deliberately simple, though often uncomfortable, way: among all possible applications, which ones truly deserve priority access to clean hydrogen? Its core principle is not to reject hydrogen, but to require policymakers to acknowledge real-world scarcity and to allocate hydrogen preferentially to sectors that are difficult to electrify, deliver high marginal decarbonization benefits, and exhibit structural necessity, rather than distributing it evenly across all seemingly feasible applications.

The Hydrogen Ladder has proven controversial precisely because it challenges the dominant narratives of recent years. In policy and industrial discourse, hydrogen has often been portrayed as an almost all-purpose solution—capable of generating electricity, storing energy, powering transport, and supporting industrial processes, and even serving as a panacea for power systems with high shares of renewables. Such "do-everything" expectations, however, frequently overlook efficiency losses, cost structures, and infrastructure realities. When clean hydrogen remains expensive and supply-constrained, attempting to advance all end-use applications simultaneously risks misallocation of resources and fragmentation of investment.

The evolution of the global hydrogen debate demonstrates that the central question has never been simply whether hydrogen should be pursued, but whether there is sufficient capacity to deploy hydrogen where it truly makes sense. Once hydrogen is treated as a scarce resource rather than a universal remedy, the focus of policy discussion inevitably shifts—from rapid expansion to patient sequencing, and from end-use enthusiasm back to the foundational work of upstream production and midstream infrastructure development. This transition may be an essential step for hydrogen to move from hype toward maturity.

Accordingly, the debate surrounding the Hydrogen Ladder is not fundamentally about supporting or opposing hydrogen. Rather, it concerns whether policymakers are willing to acknowledge that, at different stages of the transition, energy options must be prioritized and sequenced. What Liebreich emphasizes is a form of temporal judgment: some applications may be reasonable in the long term, but do not warrant priority under current conditions. This perspective closely aligns with recent analyses by the International Energy Agency (IEA) and other research institutions.

Such reflection is particularly relevant for Taiwan. As an economy with relatively limited renewable resources and a high dependence on energy imports, Taiwan's margin for trial and error in hydrogen development is far narrower than that of major energy-exporting countries. If the scarcity of clean hydrogen is overlooked and hydrogen is prematurely directed toward applications that could be served by other low-carbon technologies, overall system costs may rise while hydrogen's strategic value in truly critical industries is diluted. Conversely, by clarifying priorities and allocating limited clean hydrogen to high-value applications where hydrogen is indispensable, Taiwan has an opportunity to transform hydrogen into a source of industrial competitiveness rather than a mere policy burden.

At present, Taiwan's hydrogen strategy identifies power generation as one of three major application pillars and envisions hydrogen-based electricity accounting for 9–12% of total generation by 2050. Policy attention has also largely focused on end-use sectors such as power and transport. However, from a global perspective, most of these applications remain in research and demonstration phases, and are unlikely to achieve cost or performance advantages in the near term. If Taiwan seeks a hydrogen pathway that is both feasible and sustainable, policy thinking must shift from a single-application orientation to a system-level, integrated approach, allowing upstream production and midstream infrastructure to be established first, with downstream applications maturing and scaling at an appropriate pace. On this basis, the following three concrete recommendations are proposed.

I. Allocate Hydrogen to High–Value, Non-Substitutable Industrial and Fuel Applications

Drawing on analyses by the International Energy Agency (IEA) and BloombergNEF (BNEF), the most economically and systemically rational roles for clean hydrogen over the coming 1 to 2 decades remain concentrated in steelmaking, chemicals, high-temperature industrial processes, shipping, and synthetic fuels. These sectors are typically characterized by limited direct electrification potential, the need for reducing environments, high-temperature and high-pressure operating conditions, and extreme sensitivity to purity and supply stability—conditions under which hydrogen's chemical properties and process functions are indispensable. By contrast, allocating large volumes of hydrogen to power generation in the near term, absent clear cost or efficiency advantages, risks misallocation of scarce resources.

Semiconductors: Taiwan's Highest-Priority Sector for Clean Hydrogen Deployment

In Taiwan, beyond chemicals and steel, the semiconductor industry should be regarded as a top-priority application for clean hydrogen. Semiconductor manufacturing places exceptionally stringent requirements on gas purity and supply stability. Owing to its strong reducing properties and inherent cleanliness, hydrogen is widely used in critical process steps including wafer cleaning, chemical vapor deposition (CVD), etching, and annealing. In extreme ultraviolet (EUV) lithography, hydrogen reacts with tin to suppress contamination and preserve the quality of masks and mirrors, directly affecting yield and the stability of advanced manufacturing nodes. Production lines commonly require ultra-high-purity hydrogen at levels of 5N (99.999%) or above; even minor impurities or pressure fluctuations can compromise chip quality.

Industry assessments indicate that by-product hydrogen from Taiwan's petrochemical and semiconductor sectors already exists at meaningful scale, with an estimated industrial value of approximately NTD 61.5 billion, forming a critical foundation for localized and phased clean-hydrogen deployment. In the petrochemical sector, by-product hydrogen output exceeds internal consumption and is often combusted for heat recovery. The energy input and associated CO₂ emissions of this by-product hydrogen are substantially lower than those of hydrogen produced via natural-gas reforming or water electrolysis, making it an attractive low-carbon hydrogen source.

Hydrogen contained in exhaust gases from semiconductor manufacturing processes can also be purified and recycled, thereby reducing the carbon footprint associated with hydrogen use in fabs. However, such recovery can only offset part of total hydrogen demand, with the remainder still requiring external procurement. If this additional supply is sourced from low-carbon by-product hydrogen recovered from the petrochemical sector, the lifecycle emissions associated with semiconductor hydrogen use can be significantly reduced.

At present, science parks in southern Taiwan and Hsinchu have begun deploying water-electrolysis hydrogen production and pipeline-based supply systems. Specialized suppliers—such as Air Liquide Far Eastern (ALFE)—provide high-purity and green hydrogen through Hydrogen-as-a-Service models, helping manufacturers lower capital expenditures and enhance supply reliability. Some leading wafer fabs have replaced truck-based hydrogen delivery with pipeline supply, reducing an estimated 5,000 vehicle trips annually. This transition not only cuts emissions but also mitigates traffic and safety risks while optimizing cost structures. Looking ahead, Taiwan's hydrogen supply is expected to continue evolving toward greener sources, proximity-based industrial-park supply, and intelligent dispatch systems to support advanced manufacturing and net-zero objectives.

SAF and Hydrogen: Beyond e-Fuels, Nearly All Pathways Require Hydrogenation

Sustainable aviation fuel (SAF) is a cornerstone of aviation decarbonization, and hydrogen is indispensable across virtually all SAF production pathways. Hydrogenation steps are generally required to remove oxygen, sulfur, and nitrogen impurities, adjust hydrogen-to-carbon ratios, and ensure compliance with aviation fuel standards (such as ASTM D7566), while achieving drop-in compatibility and low-aromatic, low-sulfur characteristics. In other words, SAF entails substantial hydrogen demand, with hydrogenation representing a core cost component and a major contributor to lifecycle carbon intensity. When hydrogen is produced using renewable electricity (green hydrogen), the lifecycle carbon intensity of SAF can be significantly reduced, enhancing its sustainability performance under international certification schemes such as CORSIA and the EU RFNBO framework.

Low-Carbon Shipping: Green Methanol and Green Ammonia

Shipping is a quintessential hard-to-electrify sector, where long operating durations and heavy payloads necessitate fuels with high energy density. In this context, hydrogen can be deployed via chemical carriers:

• Green methanol (e-methanol): synthesized from green hydrogen and captured CO₂, usable both as a marine fuel and as a chemical feedstock.

• Green ammonia (NH₃): synthesized from green hydrogen and nitrogen, containing no carbon and offering higher storage and transport density than hydrogen, serving as either a fuel or a hydrogen carrier.

Directing hydrogen toward semiconductors, SAF, green methanol, and green ammonia represents a strategic allocation of scarce resources to applications with high value added and strong, non-substitutable decarbonization necessity.

II. Strengthen Hydrogen Transport and Storage Infrastructure: Integrated Ports, Industrial Parks, Pipelines, and Energy Carriers

To realize the high–value applications outlined above, midstream infrastructure must lead deployment. Taiwan should prioritize the development of hydrogen logistics hubs at ports and industrial parks, incorporating high-pressure hydrogen transmission pipelines, buffer storage facilities, loading and unloading systems, and transfer operations. These assets should be fully integrated with on-site electrolysis, purification, and recycling mechanisms within industrial zones. In parallel, international safety standards and certification frameworks should be adopted to ensure that investment risks remain manageable and transparent.

Hydrogen storage warrants particular attention. A layered strategy—by time horizon, application context, and operational scale—is recommended:

• Short term / distributed: Hydrogen storage using high-pressure cylinders or metal hydrides. These technologies are mature and can be deployed rapidly, making them suitable for refueling stations and decentralized nodes within industrial parks.

• Medium term / centralized: Storage in liquid hydrogen form or conversion of hydrogen into carriers such as ammonia or methanol. These approaches increase storage density and reduce long-distance transport costs, and are well suited to ports and large industrial facilities.

• Long term / subsurface: Taiwan should continue to explore domestic geological conditions suitable for large-scale, long-duration, and low-cost hydrogen storage—such as salt caverns used internationally. In the absence of such conditions, a "produce-and-use" model should remain the highest-priority option.

In addition, excessive reliance on imported hydrogen should be avoided, as it does little to enhance energy security. Instead, priority should be given to integrated hydrogen–renewable energy demonstration projects, whereby electrolysis and hydrogen storage are co-located at industrial parks or ports and combined with waste-heat recovery, renewable power generation, and demand-side management. Such integration can improve overall energy-use efficiency and strengthen system resilience.

III. Fuel Cell Road Transport Strategy: Avoid Expansion in Passenger Cars and Buses; Focus on Dedicated Heavy-Duty Applications

International markets have broadly converged on battery-electric passenger vehicles and electric buses as the mainstream solutions for road transport decarbonization. Taiwan should therefore refrain from large-scale expansion of fuel cell vehicles in these two segments, so as to avoid a situation characterized by insufficient infrastructure, fragmented single-site demonstrations, and an inability to amortize costs effectively.

Instead, hydrogen-based road transport should be concentrated on heavy-duty trucks operating over long distances, carrying high payloads, and running on fixed routes. Priority application environments include ports, logistics parks, and mining areas, where a "closed-network–centralized refueling–stable supply" demonstration model can be established. Such a configuration allows hydrogen demand to be spatially concentrated, refueling infrastructure to be efficiently utilized, and supply chains to achieve operational stability, thereby improving the overall economic and technical viability of fuel cell truck deployment.

IV. Strengthen Safety Measures to Mitigate NIMBY Concerns

In discussions of the hydrogen economy, hydrogen safety is an inescapable issue. The construction of hydrogen refueling stations has repeatedly encountered public opposition, particularly from nearby residents. For the semiconductor industry, safety measures associated with hydrogen use are an especially critical consideration. In this regard, the semiconductor sector's approaches to hydrogen risk assessment and safety assurance provide valuable reference points.

Professional hydrogen safety assessments should be conducted by certified and independent third parties, ensuring objective evaluation and credibility. At the same time, the proactive adoption of the latest technologies and products designed to enhance hydrogen safety should be strongly encouraged. Internationally, multiple hydrogen refueling station safety incidents have already occurred, and such cases tend to hinder broader acceptance of hydrogen and hydrogen-based applications.

Accordingly, ensuring the safety of hydrogen use sites and minimizing the occurrence of accidents represents one of the most critical prerequisites for the future deployment and social acceptance of hydrogen technologies.

Conclusion: Turning Scarcity into Strategic Advantage

Hydrogen's true value lies not in doing everything—but in doing what only hydrogen can do. By treating clean hydrogen as a scarce strategic resource and aligning its deployment with Taiwan’s industrial strengths, hydrogen can evolve from demonstration projects into a competitive industrial asset.

Early adoption of international certification frameworks (e.g., EU RFNBO), long-term contracts, and mechanisms such as Contracts for Difference (CfD) can stabilize revenue expectations, reduce financing risk, and mobilize private investment.

Using scarcity wisely is the essence of hydrogen value creation. Building a Taiwan-specific Hydrogen Ladder is therefore not optional—it is essential for ensuring that limited clean hydrogen resources support long-term competitiveness and net-zero ambitions, rather than becoming another short-lived policy slogan.

Note:

[1] Martin Tzou — Energy and Urban Infrastructure Strategy Consultant. Former Managing Director of Fluence Energy Taiwan; former APAC Director of Hydrogen and Energy Transition Marketing at Air Liquide; former roles at EDF and Business France. Advisor to the Chung-Hua Institution for Economic Research (CIER).

[2] Jung-Suen Chen — Associate Research Fellow, Green Economy Center, Chung-Hua Institution for Economic Research. Research interests include electricity markets, energy economics, and emerging technologies. Advisor to national research programs and frequent lecturer for MOEA training programs.

Martin Tzou

Energy and Urban Infrastructure Strategy Consultant. Former Managing Director of Fluence Energy Taiwan; former APAC Director of Hydrogen and Energy Transition Marketing at Air Liquide; former roles at EDF and Business France.

Jong-Shun Chen

Associate Research Fellow, Green Economy Center, Chung-Hua Institution for Economic Research. Research interests include electricity markets, energy economics, and emerging technologies. Advisor to national research programs and frequent lecturer for MOEA training programs.

More related articles